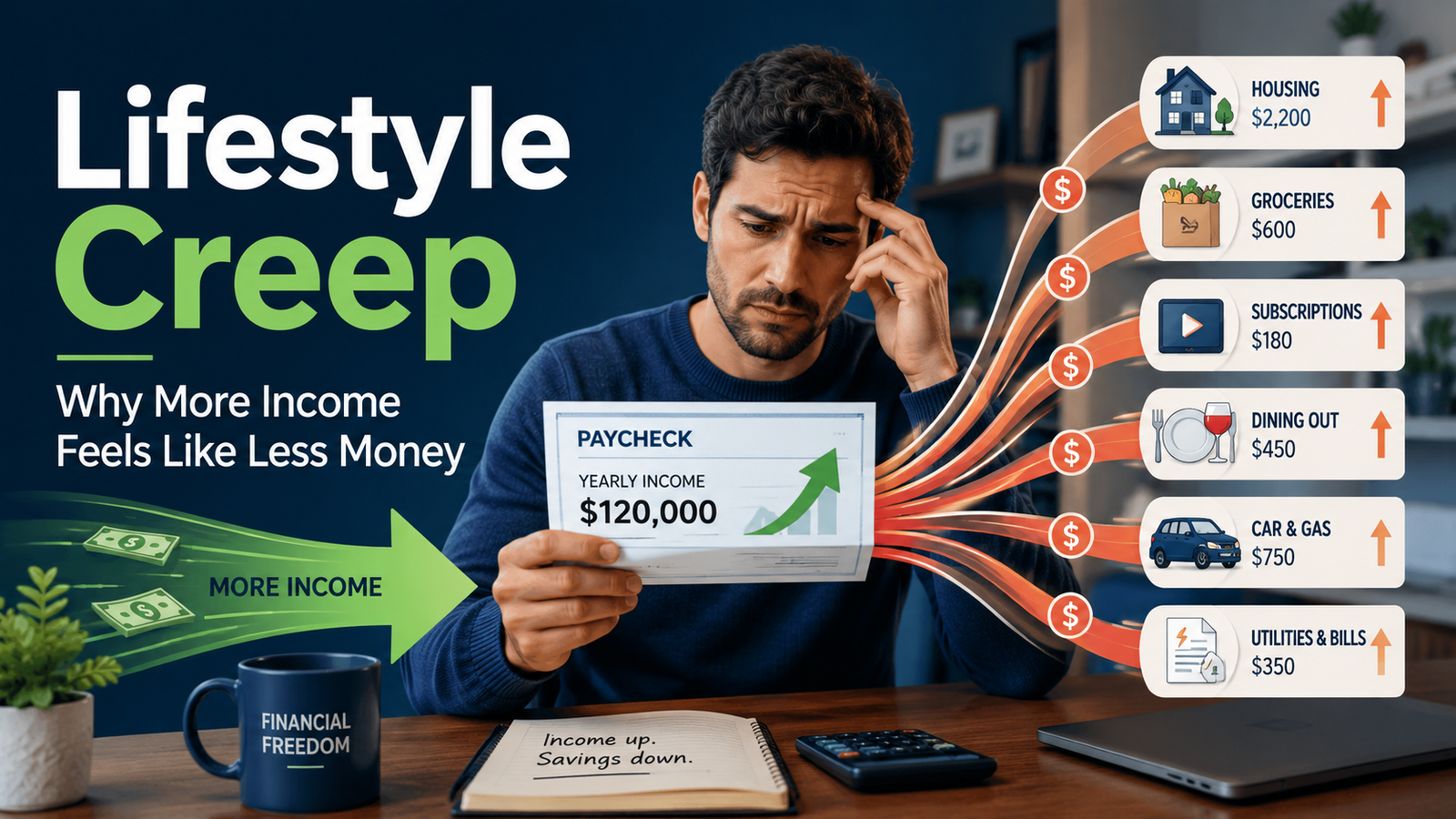

Have you ever earned more money, expected life to feel easier, and then wondered where the extra income went? That is often lifestyle creep at work. It happens when spending gradually rises along with income until the raise, promotion, or financial improvement that was supposed to create breathing room is quietly absorbed by a more expensive way of living.

The tricky part is that lifestyle creep rarely arrives with a marching band. It usually shows up through small upgrades, added conveniences, and new monthly expenses that each seem reasonable on their own. Before long, the extra income is gone, and your finances feel almost exactly as tight as they did before.

The good news is that lifestyle creep is not permanent. Once you recognize how it works, you can enjoy more of what you earn without allowing every increase in income to disappear.

What Is Lifestyle Creep?

Lifestyle creep is the gradual increase in spending that often happens as income rises.

You earn a little more, so you start spending a little more. You upgrade your phone, eat out more often, choose a nicer car, add another streaming service, or become more comfortable paying for convenience.

None of those choices is automatically wrong.

The problem begins when higher spending becomes permanent while savings, debt reduction, and long-term goals receive little or none of the additional income.

For example, imagine your monthly take-home pay increases by $500. At first, that sounds like a meaningful improvement. But then you add:

- A $75 phone upgrade

- An extra $100 in restaurant spending

- A $60 subscription bundle

- A car payment that is $175 higher

- Another $90 in miscellaneous purchases

There goes the raise.

Nothing felt extravagant on its own, but the combined effect consumed the entire increase.

Why Lifestyle Creep Happens So Easily

Most people do not wake up one morning and decide to waste more money. Lifestyle creep usually develops for reasons that feel perfectly normal.

We Quickly Adjust to a Better Standard of Living

Something that once felt like a luxury can quickly become ordinary.

The first time you pay for grocery delivery, it may feel like a special convenience. After a few months, driving to the store may start to feel like an unreasonable burden.

The same thing happens with upgraded cars, frequent restaurant meals, premium subscriptions, and higher-end services. We get used to improvements very quickly.

This is sometimes called lifestyle inflation, but the basic idea is simple: yesterday’s upgrade becomes today’s expectation.

Small Monthly Costs Do Not Feel Dangerous

Many purchases are now marketed on a monthly basis.

Instead of asking whether something costs $1,200, we are encouraged to think of it as “only $100 per month.” That makes expensive decisions feel more manageable.

The trouble is that monthly payments stack up.

A few subscriptions, a financed purchase, an upgraded phone plan, and a higher car payment can quietly add up to hundreds of dollars before the month even begins.

Spending Often Expands to Match Available Income

When money is tight, people usually pay closer attention. They compare prices, delay purchases, and think carefully about what they can afford.

When income rises, some of that caution disappears.

The bank balance looks healthier, so purchases require less thought. The extra money becomes permission to loosen spending in every category at once.

Success Can Create Social Pressure

Raises and promotions sometimes come with a sense that your lifestyle should now look different.

You may feel pressure to drive a better car, wear more expensive clothing, travel more, or spend at the same level as coworkers and friends.

That pressure may be subtle, but it can be powerful.

The problem is that other people can see what you buy. They cannot see whether you are building savings, paying down debt, or preparing for retirement.

Lifestyle Creep Is Not the Same as Enjoying Your Money

It is important to make this distinction.

The goal is not to earn more money and continue living exactly as you did forever. There is nothing wrong with improving your life when your finances improve.

Money should provide some comfort, enjoyment, and choice.

The real question is whether the upgrade is deliberate or automatic.

A planned vacation that you can afford may be a wonderful use of money. A larger home that fits your family’s needs may make sense. Paying for a service that saves time and reduces stress may be worth every dollar.

Lifestyle creep becomes a problem when spending increases without a clear decision and without leaving room for financial progress.

The issue is not that you spent more. The issue is that more spending became the default.

How Lifestyle Creep Steals Financial Progress

A raise can do several things.

It can help you:

- Build an emergency fund

- Pay off debt faster

- Increase retirement contributions

- Save for a home

- Prepare for major life expenses

- Create more flexibility in your monthly budget

But when lifestyle creep takes over, the raise may accomplish none of those things.

Your income rises, but your financial position stays almost unchanged.

That can be frustrating because you may be working harder, carrying more responsibility, and earning more money without feeling any more secure.

It is like walking up and down an escalator. You are moving, but the effort does not seem to get you anywhere.

How to Stop Lifestyle Creep Before It Takes Over

You do not need to reject every upgrade. You simply need a plan for deciding what happens when your income improves.

Decide Where the Raise Goes Before You Receive It

The best time to decide about extra income is before it reaches your checking account.

Once the money becomes part of your normal spending balance, it is much easier to use it without thinking.

Suppose your take-home pay increases by $400 per month. You might decide in advance that:

- $150 goes toward retirement

- $100 goes toward debt

- $100 goes into savings

- $50 improves your current lifestyle

That arrangement allows you to enjoy part of the raise while using the rest to strengthen your financial future.

The percentages can vary. The important part is making the decision intentionally.

Increase Savings Automatically

Automation is one of the simplest ways to prevent lifestyle creep.

When your income increases, increase your automatic transfers accordingly.

You could increase:

- Retirement contributions

- Emergency savings deposits

- Extra debt payments

- Contributions to a home or travel fund

When the money moves automatically, it does not sit in your account waiting to become another expense.

Be Careful With New Fixed Expenses

A one-time purchase affects your finances once. A fixed monthly expense follows you into every future month.

That is why new recurring payments deserve extra attention.

Before adding one, ask:

- Will I still value this six months from now?

- What is the yearly cost?

- Does this replace something else, or is it simply another expense?

- Would I still choose it if my income dropped?

A $50 monthly expense is not just $50. It is $600 a year.

That does not mean you should never spend it. It means you should recognize the full commitment.

Upgrade One Area at a Time

One of the biggest mistakes people make is improving several parts of their lifestyle at once.

A better car, a more expensive home, more dining out, upgraded travel, and new subscriptions may all arrive within a short period.

Each decision may seem manageable, but together they can overwhelm the benefits of increased income.

Choose the improvements that matter most.

You may decide that travel is important, but a luxury vehicle is not. You may prefer a nicer home while continuing to cook most meals at home.

Spending more in one meaningful area is very different from allowing every category to expand.

Keep Some Friction in Your Spending

Convenience makes spending easier, but sometimes it makes spending too easy.

Saved credit cards, one-click purchases, automatic renewals, and buy-now-pay-later plans remove the pause that once happened before a purchase.

Adding a little friction can help.

You might:

- Remove stored payment information

- Wait 24 hours before larger purchases

- Review subscriptions every three months

- Use a shopping list

- Check your account before buying

- Compare the cost with one of your goals

That small pause often separates a thoughtful purchase from an automatic one.

Review Your Spending After Every Income Increase

A raise is a good reason to review your entire financial picture.

Look at what has changed over the last few months.

Ask yourself:

- Did my savings increase?

- Has my debt decreased?

- Did my fixed expenses rise?

- Which new costs improved my life?

- Which ones barely mattered?

This is not about judging yourself. It is about noticing patterns before they become permanent.

Watch for These Signs of Lifestyle Creep

Lifestyle creep can be difficult to see because it develops gradually. These signs may tell you that it is becoming a problem:

- You earn more but still live paycheck to paycheck

- Your savings rate has not improved

- Raises disappear within a few months

- You have more subscriptions than you regularly use

- Your monthly obligations continue to rise

- You feel unable to reduce spending

- Purchases that once felt optional now feel necessary

- You depend on bonuses or overtime to cover normal expenses

One sign alone does not prove there is a serious problem. But several together are worth paying attention to.

What to Do If Lifestyle Creep Has Already Happened

Do not panic and do not try to cut everything at once.

That approach often feels like punishment, and it is difficult to maintain.

Start by identifying the expenses that provide the least value.

You may discover that you rarely use certain subscriptions, do not enjoy some of the convenience purchases you make, or have allowed spending in one category to grow without noticing.

Cutting the lowest-value expenses first is usually easier than attacking everything.

Next, redirect the money immediately.

If you cancel $80 in monthly subscriptions, move that $80 into savings or debt repayment. Otherwise, it may simply disappear into another category.

The goal is not just to spend less. It is to make sure the money produces something useful.

Use Income Growth to Create Freedom

A higher income can improve your lifestyle today and create more freedom tomorrow.

It can give you the ability to handle an emergency, leave a bad job, help a family member, retire with more confidence, or simply stop worrying about every unexpected bill.

Those benefits may not be as visible as a new car or a larger house, but they can have a much greater effect on your life.

The best approach is usually a balance.

Enjoy some of the increase. Save some of it. Use some to reduce debt. Let your present life improve without sacrificing your future.

A Simple Rule for Your Next Raise

When your income increases, pause before changing your lifestyle.

Decide what portion will strengthen your finances and what portion you are comfortable spending.

Even a simple split can make a major difference.

You might save or invest half and use the other half for current needs and enjoyment. You might choose a different percentage based on your situation.

There is no perfect formula.

The real power comes from making the decision before the money disappears.

Looking Ahead

Lifestyle creep is not caused by one bad purchase. It is the result of small increases that gradually become normal.

That is why the solution is not extreme frugality. It is awareness.

The next time your income rises, ask yourself one simple question:

How can this money improve my life today without taking away from the life I am trying to build tomorrow?

That question can help turn a raise into real progress instead of just more spending.