Intentional spending sounds simple until you try to practice it. Most people recognize the moment it describes: you check your bank balance a week before payday, and the number is lower than it should be. You pay the bills, nothing unusual happens, yet the money disappears anyway. Then the easiest explanation feels most comfortable—you just don’t earn enough. But for many households, that story doesn’t hold up under honest inspection. The real problem isn’t how much money arrives each month. It’s what happens to that money once it does.

The easy explanation is that you don’t earn enough. More income would fix it. But for many households, that story doesn’t hold up to honest examination. The real issue isn’t how much money arrives each month. It’s what happens to that money once it does.

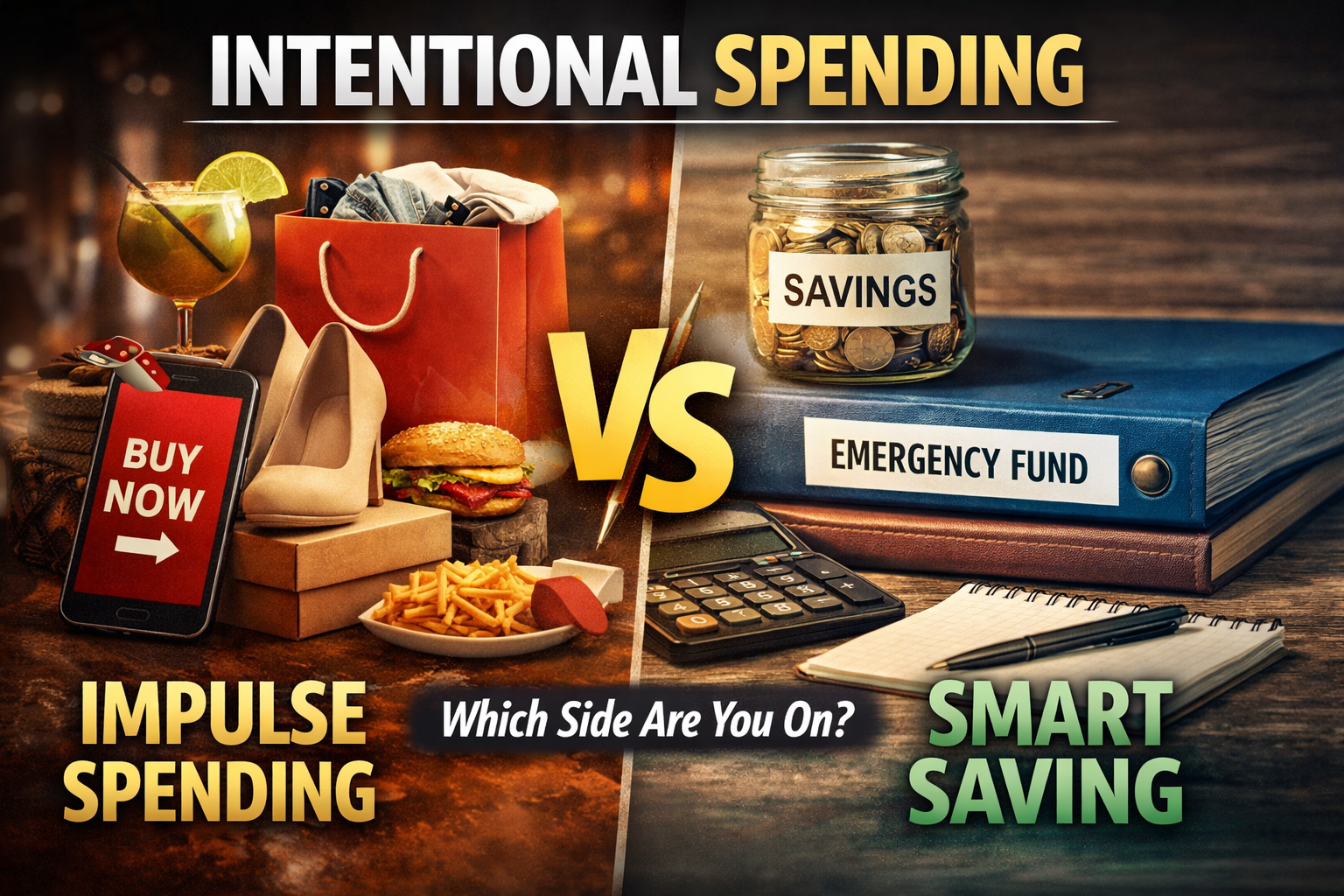

That’s the idea behind intentional spending — and it’s a simpler concept than most financial advice makes it out to be.

What Intentional Spending Actually Means

Intentional spending isn’t a budgeting system or a spreadsheet exercise. It’s really just a shift in the question you ask before you spend.

Most people ask: Can I afford this?

Intentional spending asks a different question: Is this the best use of this money right now?

That’s the whole philosophy. When you ask that second question consistently, your spending patterns start to reflect your actual priorities rather than the habits and impulses that build up quietly over time.

Spending becomes automatic faster than most people realize. The paycheck hits the account, the recurring bills take their share, and whatever remains gradually disappears through a hundred small decisions — a coffee here, a dinner out there, an online purchase that seemed like a good deal at the time. None of those individual moments feels significant. But they add up, and they add up fast.

The Non-Negotiables Come First

Before households make any interesting financial decisions, they cover fixed obligations—like rent or a mortgage, utilities, groceries, transportation, and insurance. These expenses offer limited flexibility, and they shouldn’t. Consistently paying them forms the foundation of financial stability, and that foundation matters most in the short term.

The decisions that shape long-term financial outcomes come after those are handled.

Where the Remaining Money Tends to Go

Once households cover the essentials, they reach a fork in the road—whether they recognize it or not.

One direction leads toward building something: a savings cushion, a reduced debt load, a retirement account that’s actually growing, an emergency fund that means a car repair won’t derail the whole month.

The other direction is easier and far more common. The remaining money finds its way toward convenience, comfort, and the kind of small rewards that feel well-earned in the moment — restaurant meals that become a default instead of an occasion, online shopping that fills idle time, weekend spending that outpaces the actual budget.

None of it feels reckless. That’s what makes it so effective at quietly draining financial momentum.

Then Monday comes around again, and the cycle restarts.

The Pattern That Keeps Repeating

Without any intentional direction, many households move through the same loop month after month. Income arrives. Obligations get paid. Spending absorbs what’s left. The balance drops. Stress builds. The next paycheck arrives, and the process begins again.

Over the years, this pattern leaves credit card balances unpaid, keeps savings from getting started, and creates a persistent feeling that money trouble will surface.

The pattern isn’t the result of bad values or poor character. It’s simply what happens when spending runs on autopilot.

Breaking Out of It Doesn’t Require Sacrifice

Intentional spending is sometimes confused with frugality or deprivation. It isn’t either of those things.

Nobody needs to stop enjoying their money. Life is meant to be lived, and there’s nothing productive about eliminating every purchase that brings satisfaction. The question isn’t whether you spend on things that feel good — of course you should. The question is whether those choices are being made on purpose or by default.

That distinction changes everything.

Saving a portion of each paycheck before discretionary spending begins is intentional. Planning entertainment rather than spending reactively out of boredom is intentional. Deciding which purchases genuinely matter to your life — and which ones just fill a moment — is intentional.

Small decisions made with purpose, repeated over time, build financial stability. Small decisions made without thought, repeated over time, build financial stress. Both outcomes come from the same source: the ordinary, everyday choices that don’t feel like they matter much at the time.

The One Truth That Applies to Every Household

Every family sets different priorities—based on income, obligations, and goals. No universal rule tells people how to spend money, and anyone who claims one ignores the real way people actually live.

But there is one thing that holds true across the board.

Money used without thought eventually creates pressure. Money used with intention builds options.

That’s not a complicated idea. It doesn’t require a financial planner or a complicated system. It requires one honest question asked consistently before the money goes out the door.

Is this purchase actually building the life I want — or just filling the moment?

Sometimes the answer will be: yes, this moment is worth it. That’s a perfectly good answer.

But when most purchases fall into that category by default rather than by choice, financial progress becomes very hard to find. Intentional spending is simply the habit of making that question part of the process — so that over time, where your money goes and where you actually want to go are pointing in the same direction.