Intentional Spending: Buy Better, Not Just More

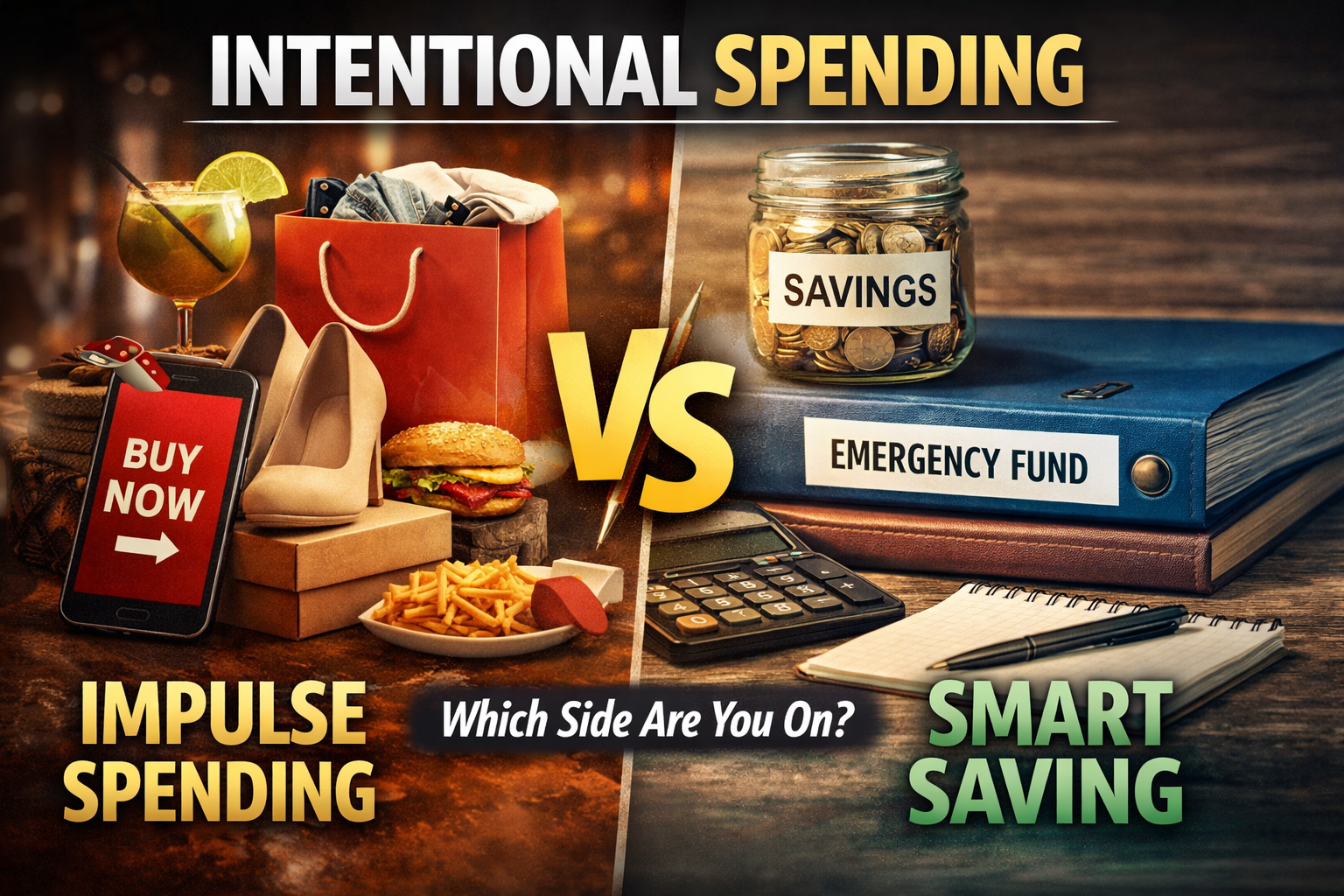

Intentional spending sounds simple until you try to practice it. Most people recognize the moment it describes: you check your bank balance a week before payday, and the number is lower than it should be. You pay the bills, nothing unusual happens, yet the money disappears anyway. Then the easiest explanation feels most comfortable—you just don’t earn enough. But for many households, that story doesn’t hold up under honest inspection. The real problem isn’t how much money arrives each month. It’s what happens to that money once it does. The easy explanation is that you don’t earn enough. More income would fix it. But for many households, that story doesn’t hold up to honest examination. The real issue isn’t how much money arrives each month. It’s what happens to that money once it does. That’s the idea behind intentional spending — and it’s a simpler concept than most financial advice makes it out to be. What Intentional Spending Actually Means Intentional spending isn’t a budgeting system or a spreadsheet exercise. It’s really just a shift in the question you ask before you spend. Most people ask: Can I afford this? Intentional spending asks a different question: Is this the best use of this money right now? That’s the whole philosophy. When you ask that second question consistently, your spending patterns start to reflect your actual priorities rather than the habits and impulses that build up quietly over time. Spending becomes automatic faster than most people realize. The paycheck hits the